Creative Real Estate Financing: From Tax Overages to International Luxury Assets

I’m Lou Brown, and I’ve been in the real estate game since 1976. In nearly five decades, I’ve seen every market cycle, every financing trend, and every strategy rise and fade. One thing that never goes out of style: creative real estate financing.

On a recent episode of The Whole Enchilada of Real Estate Investing, I sat down with K’Dia Brooks – a 28-year-old investor and military veteran who has built a portfolio that spans Section 8 multifamily apartments, probate wholesaling, international luxury properties in Italy, and tax overage deals. She did it all starting from zero, with a six-month-old baby and no outside capital.

Below are the highlights from our conversation – then the full episode. Everything in this article is drawn directly from what K’Dia shared on the show.

What Is Creative Real Estate Financing?

Solving Capital Gaps Instead of Waiting for Them to Close

Creative real estate financing is the discipline of structuring deals using capital sources beyond a standard bank loan, allowing investors to close transactions with little to no personal money down.

That includes:

- Seller carry-back financing

- Government-backed HUD loans

- Mezzanine debt,

- Tax overage capital,

- Low-income housing tax credits, and

- Cross-border equity financing.

The goal isn’t to be clever for cleverness’s sake. The goal is to close deals that standard financing would kill – and to move forward at every stage of your career, even when your balance sheet says you can’t.

“It’s not something where you’re waiting to have your money right at the perfect time… You do this along the way. I think you do real estate along the way.”

– K’Dia Brooks, Real Estate Investor

That shift – from how do I find a deal to how do I finance a deal – is what separates investors who scale from investors who stall.

The Core Tools in the Creative Financing Toolkit

Here are the “engines” that K’Dia used to generate the initial funds needed to enter the real estate without personal savings. These are also what helped her “come from nothing” to becoming a multi-national investor.

| Capital Strategy | What It Is | Key Advantage |

| Alternative Capital Sources | Entry-level funding methods to generate initial deal capital | Helps beginners create the cash needed before qualifying for larger financing |

| Government-Backed Funding | Leverage tools backed by public programs | Allows investors to close deals with far less equity than traditional lending requires |

| Layered Debt Structures | Stacking multiple financing types to fill funding gaps | Enables near or full 100% financing on large-scale deals like multifamily apartments |

| Seller Carry-Back Financing | Direct negotiation between buyer and property owner | Reduces fees, simplifies process, often saves money for both parties |

| Cross-Border Equity Financing | Leveraging international norms where seller financing is common | Expands capital flexibility beyond domestic banking limitations |

Alternative capital sources

These methods allow beginners to generate the cash required for larger, long-term deals.

This can include:

- Tax overages

- Wholesaling profits,

- Private money

These fund your entry before you can qualify for anything larger.

Government-backed funding

Government-backed funding serves as a powerful leverage multiplier in creative real estate, specifically because it allows investors like K’Dia to bypass the high equity requirements of traditional lending.

These can be:

All of which lets you close with far less equity than traditional lending requires.

Layered debt structures

Layered debt structures involve “stacking” multiple types of financing to bridge the capital gap that a single traditional lender will not cover.

As K’Dia Brooks mentions in the podcast, this strategy is essential for achieving 100% financing on large-scale deals, such as multifamily apartments.

For example, you can stack senior debt and mezzanine debt together to cover gaps that no single lender will touch alone.

Seller carry-back financing

Seller carry-back financing occurs when a buyer negotiates directly with a property owner to bypass traditional banking institutions.

This method is particularly effective because it eliminates “extra fees” and the need for agents, allowing the buyer to deal with the owner “direct”.

So the process is simple:

- Negotiate directly with the owner.

- Cut out the bank.

- Both sides often save money in the process.

In certain international markets – including Italy – seller financing is the norm, not the exception. So that’s where cross-border equity financing comes in.

In summary:

Creative financing solves one core problem: the gap between what you have and what a deal requires.

In the next sections, we’ll go over each creative financing tool in detail, covering what they are, the advantages, as well as how the process works.

Using Tax Overage Investing to Generate Capital

What Is Tax Overage Investing?

Tax overage investing – also called tax residual investing – is one of the most overlooked capital generation strategies in real estate. When a property is foreclosed and sold at auction, the sale price sometimes exceeds the amount owed in taxes.

That surplus – the overage – legally belongs to the former owner. The problem is that most counties make no effort to inform those owners that the money exists.

“That was our main thing. That’s where all of the funding is. And it’s remote, does not require you to go meet people or do anything. No driving for dollars. It’s easy.”

– K’Dia Brooks, Real Estate Investor

K’Dia and her husband discovered this strategy through their own research and internet scouting. It became their primary capital-generation engine before they moved into larger deals.

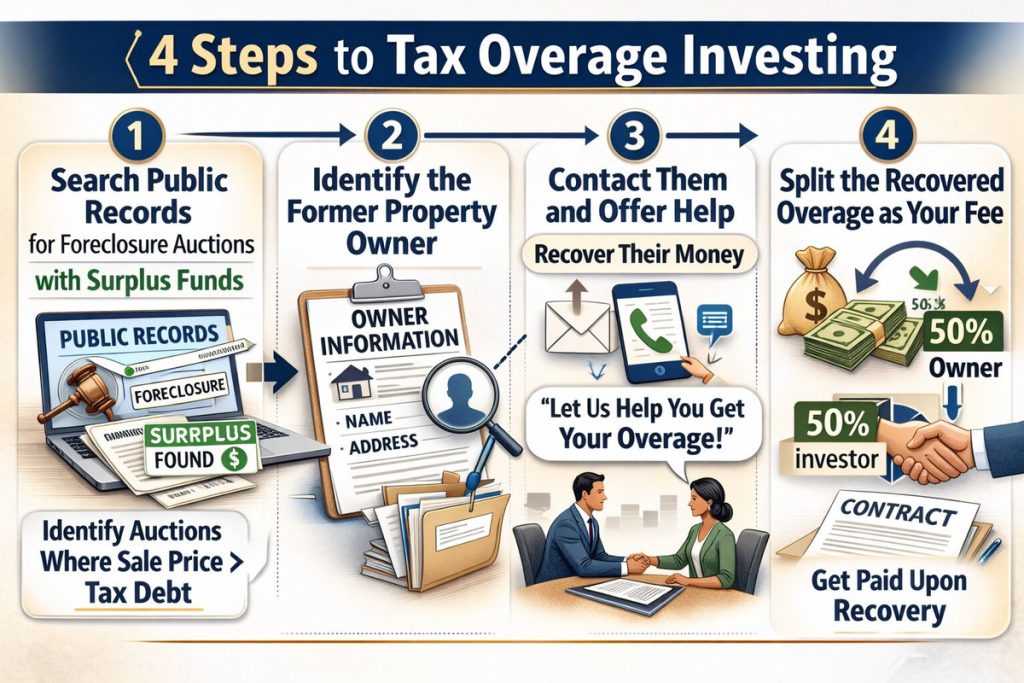

How the Process Works

- Search public records for foreclosure auctions with surplus funds.

- Identify the former property owner.

- Contact them and offer to help them recover their money.

- Split the recovered overage as your fee.

In Florida, where K’Dia operates, that money sits unclaimed for roughly three years before it’s supposed to move to the state treasury. In practice, as K’Dia noted, it often just gets absorbed into that county’s slush fund.

Why Counties Don’t Notify Owners

In our podcast episode, K’Dia expressed great surprise that local governments put “absolutely no effort into reaching out to these owners” to inform them that they have money, sometimes as much as $50,000, sitting at the tax office after an auction.

But the counties generally do not notify owners of these tax overages because the lack of awareness allows them to eventually claim the funds for themselves.

In Florida, the money just sits there for about 3 years before it is supposed to go to the state treasury office, where they can go access unclaimed funds. But really, what happens is it just gets absorbed into that county slush fund.

That gap is exactly where this strategy lives.

“You can stay in one state, even in a few counties, and never run out of opportunities.”

– K’Dia Brooks, Real Estate Investor

Competitive Positioning: Medium Counties Win

Rather than chasing six-figure overages in Miami or Orlando – where larger players like attorney Bob Diamond are already operating – K’Dia’s team targets medium-sized overages, nothing under $30,000. At four or five deals per month in that range, the revenue adds up without the competition.

Counties surrounding Orlando and areas like Marion County (Ocala) upload new PDF sheets two to three times a week, each adding 100 to 200 new entries of properties that have been foreclosed, without depleting.

This is a capital-generation phase, not an end strategy. It builds the war chest that funds everything that comes next.

How HUD 100 Percent Financing Changes the Game

The 95% Starting Point

When K’Dia and her husband picked up a book by real estate developer Jorge Perez from their local library, they found something that changed their trajectory: HUD will finance 90-95% of qualifying multifamily deals.

“So we were continuously learning. I think we picked up a book by Jorge Perez, and he’s like a developer, and he introduced us to section 8 HUD financing. And we were like ‘Oh wow, like HUD will finance 95% of these deals.’”

– K’Dia Brooks, Real Estate Investor

For investors with limited capital, that number alone is significant. But then came the next discovery – how to push past 95% and reach 100%.

Stacking Tax Credits to Reach 100%

This is where the real estate capital stack comes into play. Here’s how the layers stack together:

| Layer | Source | Coverage |

| Senior Debt | HUD Loan | 95% |

| Equity Layer | Low Income Housing Tax Credits (LIHTC) | Fills part of gap |

| Gap Layer | Mezzanine Debt or Opportunity Zone Funds | Fills remainder |

Layer low income housing tax credits on top of the HUD loan. Add opportunity zone fund incentives depending on the location, and you have a real path to closing a deal with no money of your own.

“You tack on a few low-income tax credits and now you can fund deals 100%.”

– K’Dia Brooks, Real Estate Investor

That combination is what moved K’Dia and her husband out of wholesaling and into multifamily. Once they understood what the capital stack could do, the strategy was clear.

Mezzanine Debt Real Estate (Filling the 25% Gap)

How Mezzanine Debt Works

Traditional lenders typically fund 70–75% of a deal’s value, which means there’s always a 25–30% gap standing between you and a closed deal. Mezzanine debt fills that gap. Mezzanine investors step in as a second-position capital layer – not senior lenders, but not equity partners either.

“You are normally given a 70-75% LTV whereas Mezzanine debt investors are basically investors that come in and take care of the other 25%.”

– K’Dia Brooks, Real Estate Investor

The structure looks like this:

- Payments are interest-only during the loan term

- The term is typically 3–5 years

- At the end of the term, a balloon payment is due in full

The Risk You Have to Plan Around

That balloon payment is where investors get into trouble without a clear exit strategy. K’Dia’s book, Fundamentals of Financing, available on Amazon, walks through exactly how to use mezzanine debt strategically – building the cash flow or exit plan to handle the balloon before it arrives.

“Usually, however, you’re paying interest only on these and it’s usually for a shorter time about 3-5 years, where after the 5 years, if you’re paying the interest only on it, it’s a balloon payment all at once. So that’s something to use strategically, so that you can make sure you have the cashflow, the funding.”

– K’Dia Brooks, Real Estate Investor

Mezzanine debt is an advanced-level tool in the creative financing toolkit. Pair it with the right deal and the right exit plan, and it closes transactions no traditional lender would touch. Pair it wrong, and that balloon becomes a boulder.

“Your exit strategy is to be able to pay off the mezzanine debt at the time of that balloon period.”

– K’Dia Brooks, Real Estate Investor

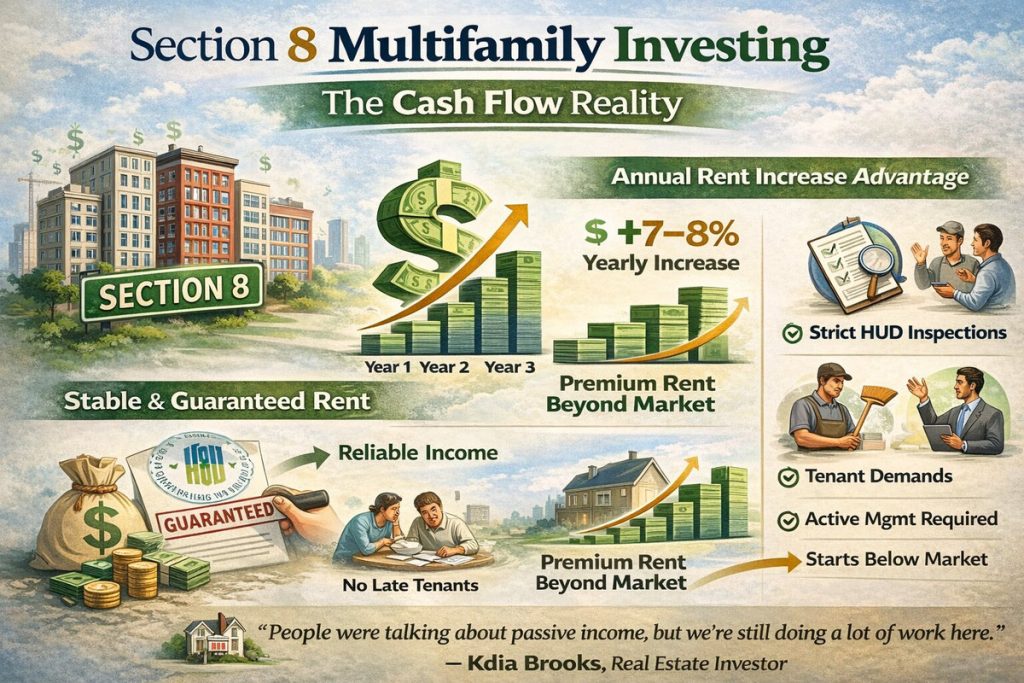

Section 8 Multifamily Investing – The Cash Flow Reality

Section 8 multifamily investing means buying apartment buildings where the government (through HUD) pays a guaranteed portion of the rent every month. Instead of hoping tenants can cover their rent, you’re collecting from a federal program that doesn’t miss payments.

The 2% Mortgage Tax Incentive

In the United States, seller financing real estate deals are a negotiation. In Italy, they’re practically the default.

The reason is, both the buyer and the seller are hit with a 2% mortgage tax on the purchase price if they go through traditional financing. That penalty creates a direct incentive to bypass banks entirely and deal owner to owner.

“It’s more common here because both buyer and seller are penalized with a mortgage tax.”

– K’Dia Brooks, Real Estate Investor

No agents. No extra fees. No mortgage tax. Both parties save, and the deal gets done directly.

The 1.2 Million to 550K Example

K’Dia and her husband found a historic property in Italy originally listed at 1.2 million euro. After negotiating directly, they purchased it for 550,000 euro – with a 60,000 euro down payment and seller-carry-back financing on the remainder.

That’s a deep discount plus seller financing plus a low down payment – three creative financing wins in one transaction.

“It was a no-brainer for us.”

– K’Dia Brooks, Real Estate Investor

This historic home they purchased is now operating as a luxury wedding venue and exclusive accommodation property. More about that in the next sections.

| If you’re an investor looking to close more deals, I put together a free Cost to Sell Worksheet that helps you walk sellers through exactly what a traditional sale is costing them – commissions, closing costs, mortgage taxes and all. Once a seller sees those numbers laid out, the case for working directly together writes itself. You can show them exactly what they save, and you both benefit. |

International Real Estate Investing – A Luxury Yield Model

Tourism Arbitrage at Its Finest

K’Dia and her family didn’t discover Italy as an investment market from behind a spreadsheet.

They were already traveling there regularly, staying in short-term rentals for three months at a time – spending as much as 15,000 euro to stay at their apartment for 3 months.

Walking the streets, they noticed real estate listings posted directly in agency windows: 60,000 euro, 70,000 euro for apartments. They were paying nearly that much in a single off-season rental.

“But these apartments, most of them post their listings right on the window… these for 70,000 euro, 60,000 euro. And they just got 15,000 from our short season stay. So we were like, ‘hey, tourism pays here.’”

– K’Dia Brooks, Real Estate Investor

That’s when we realized investing in real estate in Italy made sense not just as a lifestyle play, but yield play.

The Wedding Venue Model

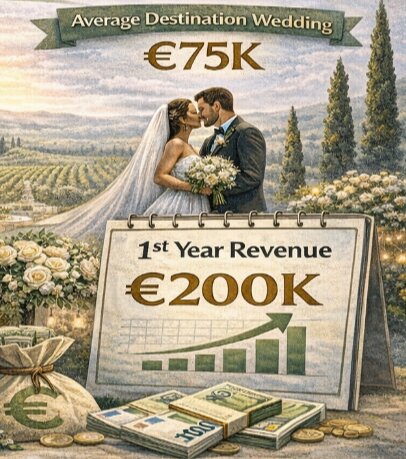

The historic home K’Dia purchased is now operating as a luxury wedding venue and exclusive accommodation property. The average destination wedding in Italy runs 75,000 euro – with the venue being the bulk of that cost, alongside food and catering.

With a 60,000 euro down payment, K’Dia projected at least 200,000 euro in year-one revenue from weddings alone.

“The first year, we’ve covered (our investment) times three, just in weddings alone, because the home is a wedding venue. And it amazed us to see what people actually paid for destination weddings.”

– K’Dia Brooks, Real Estate Investor

Building the On-Site Team

Running a venue like this requires a real team. Since arriving in Italy, K’Dia has been building out full operations on-site:

- Luxury travel concierge who doubles as the in-house wedding planner

- Catering team

- Gardeners and grounds staff

- Full accommodation management for Airbnb-style and corporate rentals

Tax Incentives for Tourism in Italy

Italy’s corporate tax rate sits at around 24%, but the government actively subsidizes and incentivizes tourism and agritourism businesses. It functions similarly to agricultural tax incentives in the U.S. – the government wants this sector to thrive, and it pays investors to support it through deductions and program incentives.

Investing in real estate in Italy through a tourism model puts you in a category the Italian government actively wants to grow.

Build to Rent Strategy – The Next U.S. Shift

The Demand Shift Driving This Strategy

For their U.S. strategy, K’Dia and her husband are stepping back from acquisitions while the market settles and pivoting toward development – specifically the build-to-rent model.

What is Build to Rent?

Build-to-rent means constructing homes specifically to rent out rather than sell. The model targets renters who want the space and amenities of a single-family home – a garage, a backyard, room for kids and pets – but aren’t ready or willing to take on a mortgage.

These people are not buying because they can’t. Many of them are just choosing not to. The build to rent strategy is designed directly for that tenant.

“We’re just not focused on acquisitions right now. I want to wait for the U.S. to calm down a little bit on the acquisition front. But I think, moving forward our goal is development, and mainly into build-to-rent.”

– K’Dia Brooks, Real Estate Investor

Why Development Beats Acquisitions Right Now

Development offers something that acquisitions in an overheated market can’t: control over the cost basis. You’re not bidding against a crowded field for existing inventory at inflated prices. You’re building the product the market wants, at a cost you control, for tenants who are ready and waiting.

This is the next phase of the capital progression model.

The Capital Progression Model (Tie Everything Together)

A Ladder, Not a Shortcut

Creative real estate financing works best when you treat it as a progression – each phase building the capital, leverage, and cash flow that funds the next.

| Phase | Strategy | Goal |

| Phase 1 | Tax overages / wholesaling | Capital creation – build your war chest |

| Phase 2 | HUD + LIHTC + mezzanine debt | Leverage expansion – close without large cash reserves |

| Phase 3 | Section 8 multifamily | Cash flow stabilization – government-backed, rising rents |

| Phase 4 | Build to rent + international assets | Yield optimization – higher returns, scalable models |

The Philosophy Behind the Progression

Each phase uses creative financing differently.

- Tax overages are a capital-generation engine.

- HUD and mezzanine debt are leverage multipliers.

- Section 8 is a cash flow stabilizer.

- Build to rent and international assets are yield optimization plays.

The tools change. The philosophy stays the same: find the capital gap, structure around it, and move forward. That’s what creative real estate financing actually means in practice.

Frequently Asked Questions About Creative Real Estate Financing

What is creative real estate financing?

Creative real estate financing uses non-traditional capital sources – seller financing, government-backed HUD loans, tax credits, mezzanine debt, and tax overages – to fund deals that standard bank loans won’t cover. The goal is to close despite capital gaps, not wait for them to disappear.

Is tax overage investing legal?

Yes. Tax overage investing involves working with public records and unclaimed surplus funds that legally belong to former property owners. Rules and earning caps vary by state and county, so learn the specific regulations in your market before getting started.

How does HUD 100 percent financing work?

HUD loans can cover up to 95% of qualifying multifamily deals. Layer low-income housing tax credits and opportunity zone funds on top of that, and it’s possible to reach full 100% financing through the right capital stack structure.

What is mezzanine debt real estate?

Mezzanine debt fills the gap between a senior lender’s 70–75% loan-to-value and the full deal price. Mezzanine investors cover the remaining 25–30% – typically through interest-only payments with a balloon payment due at the end of a 3–5 year term.

Is Section 8 investing profitable?

It can be – especially with HUD’s 7–8% annual rent increases that over time can push rents above market rate. The trade-off is active management, annual inspections, and tenant challenges. The numbers need to be strong enough to justify the work.

Can you use seller financing internationally?

Yes. In Italy, seller financing is more common than in the U.S. because both buyers and sellers face a 2% mortgage tax on the purchase price when using traditional financing. That penalty creates a direct incentive for direct, owner-to-owner deals.

Is investing in real estate in Italy a good idea?

For the right investor, yes. Italy offers low acquisition prices relative to other Western European markets, high tourism demand, strong government support for tourism businesses, and favorable seller financing conditions that aren’t as common in the U.S.

What is a build to rent strategy?

Build to rent means developing residential properties specifically to lease – not sell. It targets the growing segment of renters who want the lifestyle of a home without the commitment of ownership. Development gives investors control over cost basis in a way that acquisitions in competitive markets don’t.

How do beginners start with creative financing?

Start with capital generation – wholesaling or tax overage investing – before attempting HUD or mezzanine deals. Build your knowledge base and your capital at the same time. Learn the financing structures as you go, and don’t wait for perfect conditions to get started.

🎙️ THIS PODCAST IS PRODUCED BY ICONS OF REAL ESTATE

Icons of Real Estate – #1 Real Estate Podcast Network

Apply to Be a Guest on The Whole Enchilada of Real Estate Investing Podcast

Real estate is evolving. Capital is shifting. Strategies that didn’t exist five years ago are closing deals today.

If you serve the real estate industry – through staffing, lending, brokerage, technology, or advisory – and you’re actively helping investors grow smarter, not harder, we want to hear from you.

Apply to be featured on The Whole Enchilada of Real Estate Investing podcast and share your insights with a community of investors who are ready to act.

Marigona Gllarevaa – Jan 01, 1970