Generational Wealth and Avoiding Cash Flow Mistakes for Multifamily Investors With Jon Swire from The Agency

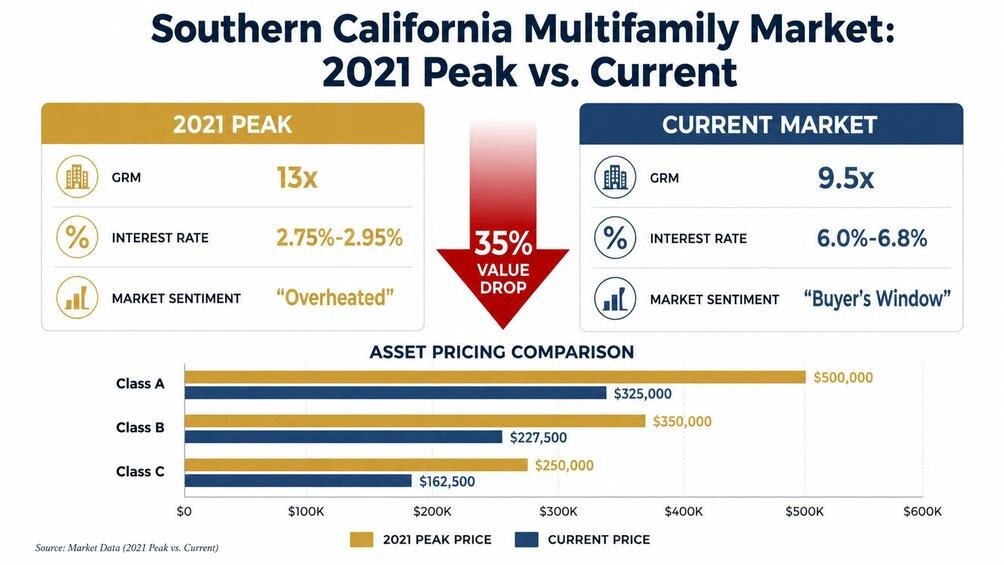

Most multifamily investors fail at cash flow, not because they pick the wrong building, but because they never learned how debt actually works against them when interest rates shift. Apartment values in Southern California have dropped 35% since their 2021 peak, posing challenges for overleveraged owners but offering a strong buying opportunity.

Here’s a snippet of our conversation:

On a recent episode of The Whole Enchilada of Real Estate Investing, I sat down with Jon Swire from The Agency. He’s a top-producing advisor specializing in Los Angeles multifamily properties, to break down exactly how prepared investors can turn this disruption into lasting wealth.

Listen to the full episode:

Navigating Shifting Economic Landscapes with a Multifamily Market Authority

Jon is not your average broker. He holds an engineering degree and an MBA, and he will tell you straight that math is his love language. Over 25 years in the business, he has helped clients buy and sell over 500 buildings worth more than $1 billion in total transaction volume. He personally owns over 15 buildings in California, most of them in the Long Beach area.

On top of that, he has been teaching real estate investment education at UCLA Extension since 2006, covering everything from capitalization rates to leveraged equity yields. His Real Estate Investment Analysis curriculum at UCLA Extension has become a foundational course for aspiring investors across Southern California.

What I appreciated most about our conversation was how Jon combines academic theory with street-level execution. He is not just teaching formulas in a classroom. He is applying them every week in live transactions. That rare mix aligns perfectly with my own philosophy of buying right, buying cheap, and buying creatively.

Capitalizing on the Historic 35% Southern California Multifamily Market Value Drop

We’re in a remarkable buying window, with Southern California multifamily prices down about 35% from their 2021 peak. This is huge for agents and investors who grasp valuation metrics.

Jon put it plainly during our conversation: deals that were trading at 13 times gross rent multiple are now trading around a 9.5 GRM. That kind of pricing correction is a massive advantage for anyone deploying fresh capital to secure generational assets at a steep discount.

This correction did not happen because tenants stopped needing housing. The core of this market shift is rooted in a sudden repricing of assets driven by macro-level interest rate pressures. The Federal Reserve’s aggressive tightening cycle sent commercial mortgage rates from below 3% to north of 6% in a matter of months, and the apartment sector absorbed that shock directly through compressed property values. According to the National Association of Realtors commercial real estate research, multifamily cap rates have expanded meaningfully since 2022, reflecting this repricing across every major metro.

Jon specifically pointed to Long Beach, California, as a market worth watching. While the entire state of California operates under statewide rent control, Long Beach does not impose additional local rent control restrictions beyond the state guidelines. That regulatory environment gives landlords more operational flexibility, and the location sits right on the water.

For investors evaluating where to deploy capital, that combination of regulatory advantage and coastal demand makes it a compelling target. Understanding how real estate outperforms traditional stock market investing over long holding periods makes this pricing correction even more significant for wealth builders.

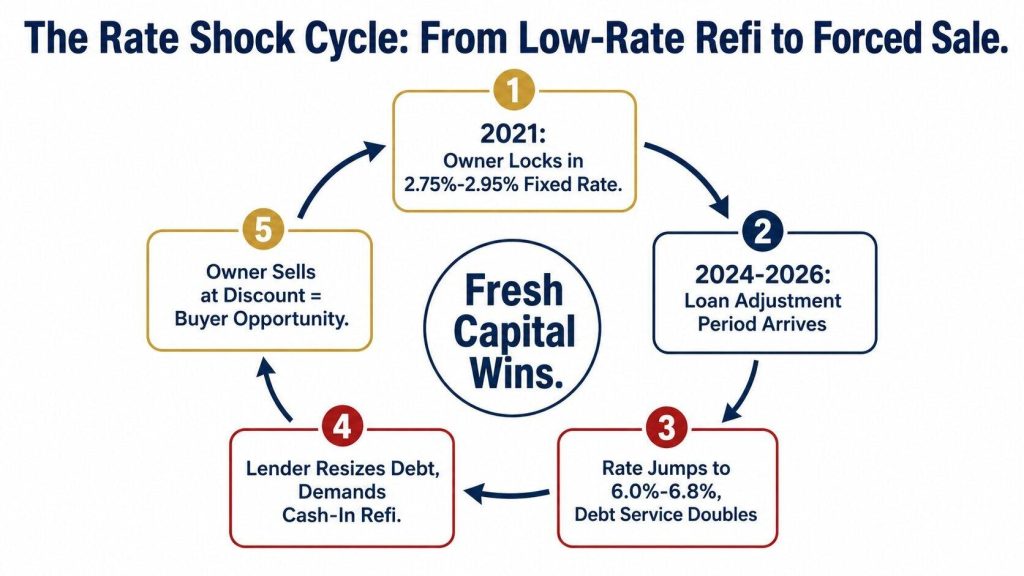

How the Rate Shock Explosion Triggers Desperate Cash-In Refi Scenarios

The distressed inventory is due to 2021 debt choices, with low-rate loans now facing doubled payments as rates rise to 6%-6.8%, wiping out cash flow.

Jon explained this dynamic clearly during our conversation. When lenders review annual reporting and see that a property’s net operating income can no longer support the existing loan at the new rate, they do not simply look the other way. They resize the debt to meet strict debt coverage requirements.

“Lenders in a lot of cases are resizing the debt to meet the DCR, the debt coverage requirements. So what a lot of borrowers don’t understand is the lender’s gonna come knocking and say, ‘Hey, we’re looking at your annual reporting. Your loan of 1.5 million covered and worked at a 3% rate, but at a 6% rate, the building doesn’t generate enough net operating income to support this debt coverage. So we need you to pay the loan down from 1.5 to 1.2 million.’ Now the borrower is ‘Wait a minute, I don’t have 300K’ So that’s what’s gonna cause them to come to the market and just say, ‘Uncle, I give up. I gotta sell this thing.'”

That scenario is the definition of a cash-in refi. The lender tells the borrower to bring hundreds of thousands of dollars to the table just to keep the property. If a small mom-and-pop landlord or syndicator lacks the liquid capital to instantly pay down that loan balance, they have no choice but to wave the white flag and bring the property to market.

This structural debt pressure creates significant opportunities for investors with fresh capital reserves, referred to as “fresh powder,” representing an ideal position to be in currently. Disciplined buyers with cash can acquire quality apartment buildings at steep discounts while overleveraged owners struggle to meet lender demands. Jon’s multifamily apartment brokerage practice gives him a front-row seat to these transactions as they unfold across the LA market.

Office space in Los Angeles is now selling for 20 to 30 cents on the dollar compared to peak prices, with some buildings dropping from $400 to under $100 per square foot. Rising interest rates and remote work have hit office valuations hard. Jon and I agree: stick to multifamily. Apartment leases are straightforward, unlike complex commercial leases.

Tattooing the Cash Flow Fundamentals on Your Forehead for Long-Term Freedom

To scale a resilient real estate portfolio, focus on predictable cash flow. Real estate isn’t an appreciation lottery; it’s a financial tool for steady retirement funding.

Jon emphasizes to his UCLA students: always expect cash flow with a traditional five-plus-unit multifamily property and a conventional commercial loan. The debt coverage requirements ensure the property generates enough income to cover the debt.

I always emphasize my core philosophy of cash now, cash flow, and cash forever. To achieve this, your first property cannot be treated as your final destination. It is simply step one on a generational ladder. True wealth scaling occurs when you purchase cash-flowing assets, stabilize their performance, and eventually execute a 1031 exchange into larger portfolios. Jon and I both see the same endgame: get to 50 to 100 units, and now you have enough passive income flowing in to make a real difference in your life and your family’s future.

Jon uses Excel with clients, guiding them through numbers. Many initially don’t understand, so he focuses and guides them, aiming for a 5% to 6% cash-on-cash return. If they push 7 or 8, that is a bonus. But 5% to 6%, slow and steady, wins the race every time. Building massive passive income from rental properties is the foundation of this entire approach.

Unmasking the Value-Add Myth and Navigating the Nightmare of Forced Capital Expenditures

Many agents and investors are enamored with heavy value-add deals, thinking renovating dilapidated buildings leads to quick wealth. From 2015 to 2020, Jon’s team rehabbed nearly 1,000 units in Long Beach, benefiting from predictable costs and wide margins.

That window has closed. In today’s market, skyrocketing material prices, contractor instability, and severe municipal utility delays mean that the juice is rarely worth the squeeze. Jon shared a painful example from his own portfolio that drives the point home.

“We’re on a deal right now, we’re into year… We just rolled past year number four, where we’re tied up with LADWP updating the electrical on a project, and we can’t get a transformer placed. So we have a building now that’s been vacant for four-plus years. The carry cost alone on that is a couple of hundred grand a year in debt service. When you look at the deal from cradle to grave, it’s very difficult to envision where it’s gonna turn out to be anything other than, I don’t wanna say an unmitigated disaster, but just a mess.”

Four years of vacancy. A couple of hundred thousand dollars a year in carry costs. And the project is still not generating a single dollar of rental income. That is the reality of heavy value-add in the current environment. When a property sits vacant for years waiting on local municipal approvals or utility upgrades, the holding costs will destroy your projected returns faster than any rent increase can recover them.

Jon suggests avoiding heavy rehab projects. Verify properties by checking utility bills, hiring independent roofers, and inspecting sewer lines. Budget only for existing maintenance. Ideally, purchase if renovations are seller-funded and yields meet your minimum rates. You skip the brain damage entirely. Knowing what to look for when evaluating property repairs before purchasing can save you from exactly the kind of nightmare Jon described.

Jon’s read on practical real estate investment strategies in his book, “There’s No Free Lunch in Real Estate,” covers these due diligence principles in detail. The title alone tells you everything about his investing philosophy: there are no shortcuts, and every deal must be earned through disciplined analysis.

Why Overcoming America’s Deep Financial Literacy Crisis Changes Everything

This conversation reinforced my conviction that the single biggest barrier holding back talented individuals from building real estate wealth is the profound lack of basic real estate financial literacy in our country. Mainstream education fails to teach leverage, debt optimization, and balance sheet structuring. Many see real estate debt as risky, not knowing it can be offset by tenant income.

Jon feels this deeply. He has argued for years that financial literacy should be taught in high school, in college, to doctors, to lawyers, and to everyone in between. He sees it every day in his practice.

“Most people in the United States lack basic financial literacy, okay? This is a class I’ve always argued should be taught in high school, in college, to doctors, to lawyers, just to everybody. It’s amazing how many people don’t understand basic stuff. They’re scared of making the decisions that to you and me are no-brainers. I carry close to $40 million in real estate debt on my balance sheet, which, to a lot of people, is holy cow, that’s a crazy amount of money. But what people don’t understand is that on the balance sheet, that comes with income to offset all those debt payments.”

$40 million in real estate debt can be daunting, but when it’s backed by income-producing apartments, it’s manageable. The debt is offset by rental income that covers payments.

This realization fundamentally shapes my own approach to real estate mentoring. I have always believed that comprehensive real estate investing education is what separates successful investors from those who stay stuck on the sidelines. Set realistic short and long-term goals based on family liabilities. Align with a mentor to stay focused and manage transactions effectively.

Jon jokes that he is his clients’ “real estate rabbi.” I love that. When you find the right guide, someone who has genuinely done the deals and survived the cycles, you stop fearing the raw numbers and start mastering them. Jon offers personalized real estate mentoring sessions for investors who want that level of hands-on guidance. Combined with his brokerage expertise and teaching background, he brings a depth of support that most advisors simply cannot match.

Want to hear my entire conversation with Jon Swire from The Agency on why most investors fail at multifamily cash flow? Listen to our podcast episode!

FAQ Section

How does a gross rent multiple (GRM) impact my multifamily property evaluation?

The gross rent multiple is a metric used to quickly gauge the price of a multifamily property relative to its gross rental income. Divide the property purchase price by its annual gross rent. A lower GRM suggests a better price per rental income, indicating stronger potential yield and quicker profitability.

What exactly is a cash-in refi, and why does it occur in commercial real estate?

A cash-in refi occurs when a commercial property owner must inject additional personal cash into a property to secure a new mortgage. When property values decline or interest rates increase, net operating income may fall short of the lender’s debt coverage ratio, requiring the borrower to pay down the principal to bridge the gap.

Why is office space collapsing while multifamily apartment investing remains resilient?

Office space values have plummeted due to reduced demand from remote work and rising vacancy rates, coupled with higher interest rates. In contrast, multifamily apartments meet essential housing needs, maintaining steady demand and attracting capital, even amidst economic turbulence.

Apply as a Guest Speaker

The multifamily real estate arena is shifting at a rapid pace. Interest rate adjustments are reshaping portfolios, equity margins are compressing, and unique buying windows are appearing across major metropolitan markets. If you are actively operating in today’s landscape, deploying innovative financing, or executing creative real estate strategies, we want to hear your story.

Whether you work in construction, finance, brokerage, or development, and you are solving real problems in the industry, we would love to feature you.

Marigona Gllarevaa – Jan 01, 1970