Tax Secrets for Real Estate Investors with Paul Graham, Tax Strategist and Serial Entrepreneur

High-income earners and real estate investors keep more of their wealth by using a strategic approach. They align loss with income and direct savings into purpose-driven assets rather than lifestyle expenses.

That single idea anchored my conversation on The Whole Enchilada of Real Estate Investing, where I sat down with Paul Graham, a tax strategist, serial entrepreneur, and the founder of Octane and The Investor’s Guide to Joy.

Paul and I had a little chat on my channel, and here’s a snippet of our conversation.

What follows are the insights that stood out most, paired with the practical moves you can put to work this year.

Aligning Your Portfolio With a Purpose-Driven Heart Posture

I expected our talk to live entirely in the weeds of wealth preservation. Instead, Paul opened with a phrase I had never heard before: “heart posture.” As real estate professionals, we get pulled toward cap rates, cash flow, and net worth milestones. Paul’s point cut deeper. The investments we make touch real people, and our underlying intention shapes how we hold up when markets turn.

Whether you serve families as a certified affordable housing provider or scale a business as a high income earner looking to reduce taxes, your motive drives your staying power. Paul put it plainly when he described the shift he sees in successful founders.

“My belief goes further and farther than just my own ego. Focusing just on income, net worth, or status has its kind of runway. I tend to see about the eight-figure net worth level, people then try to be like, ‘What’s my purpose? I have enough.’ It’s more the human being as opposed to the human doing.”

That framing matters because of where it leads. When you stop chasing status, you free up capital and attention for moves that actually compound. Research on financial well-being from the Consumer Financial Protection Bureau backs this up, showing that security and a sense of control over money predict well-being far more reliably than raw income. Paul has lived that lesson, and he writes about it through his work at The Investor’s Guide to Joy.

Mastering Active vs Passive Income Tax Rules to Protect Your Revenue

The most expensive mistake I see investors make is trying to wipe out a W-2 salary with losses from a passive rental. It does not work, and the active versus passive income tax rules explain why.

For high income earner tax reduction to work legally, you must match your losses to the right income bucket. Paul named this blind spot directly during our talk.

Paul named this blind spot directly during our talk.

“There’s a difference between active and passive income, and also being able to offset those differently. Sometimes people invest in real estate and take passive losses, but then try to offset their corporate salaries. The short answer is that it doesn’t work. So you need passive losses to offset passive income and active losses to offset active income.”

The IRS draws this line under Section 469. As the agency lays out in Publication 925 on passive activity and at-risk rules, rental real estate is treated as passive by default, even when you materially participate, unless you qualify as a real estate professional. Passive losses can only offset passive income. To apply real estate losses against active income, like wages or bonuses, you need a specific vehicle, such as a short-term rental you manage or a Real Estate Professional Status.

Active Income vs. Passive Income at a Glance

| Category | Example Sources | Offset Rule |

| Active Income | Wages, business profit, managed short-term rentals, oil and gas, film credits | Offset only with active losses |

| Passive Income | Traditional long-term rentals, limited partnerships | Offset only with passive losses |

Here is how to put this to work without guesswork. First, audit your revenue streams and sort every dollar as active, passive, or portfolio income before you plan year-end deductions. Second, if you need large active losses fast, consider alternative plays like oil and gas or film credits, both of which Paul has used himself. Third, bring in a specialized CPA early, well before you sign on a major acquisition.

The National Association of Tax Professionals maintains directories that make finding a qualified real estate specialist straightforward. Members of NATP specialize in various industries, including real estate, and assist approximately 10 million clients annually.

Optimizing Short Term Rental Tax Strategies and the Reality of House Hacking

Paul scaled fast, and he was candid about both the upside and the headache.

“From a span of 18 months, I went from a cute little condo to three single-family homes plus land next to them and over 10,000 square feet of property. And those properties are effectively short-term rentals. Through short-term rentals, I can offset different taxes, basically to make it short and sweet. But man, it is not my ideal type of investment and strategy because there’s a lot of nuance or headache around it, so I’ve had to hire property managers. My point is that there are different ways to strategically offset taxes or prepare for tax season, but it’s really the idea of what you are optimizing for, both in terms of lifestyle, but also your future.”

This is where short term rental tax strategies earn their reputation. When the average guest stay runs seven days or less, and you materially participate, the IRS stops treating the property as a passive rental, which means the losses can offset active income. Investors pair that with cost segregation studies and accelerated depreciation to front-load deductions. The Tax Foundation provides a solid background on how depreciation provisions like these shape investor behavior.

The warning inside Paul’s story is the part most people skip. Tax advantages should never blind you to operations. Hospitality properties throw off strong cash flow and real tax benefits, but they demand intense day-to-day management. Plan your operational infrastructure from day one.

House hacking real estate strategy, whether you rent out spare rooms or run a pad-split setup, works beautifully as a launchpad to cut living costs and stack capital. The endgame, though, is converting those short-term gains into automated systems or long-term wealth preservation vehicles.

For a deeper dive into oil and gas syndications, family office structures, and advanced tax strategies, I recommend exploring Paul’s collection of advanced real estate investing e-books.

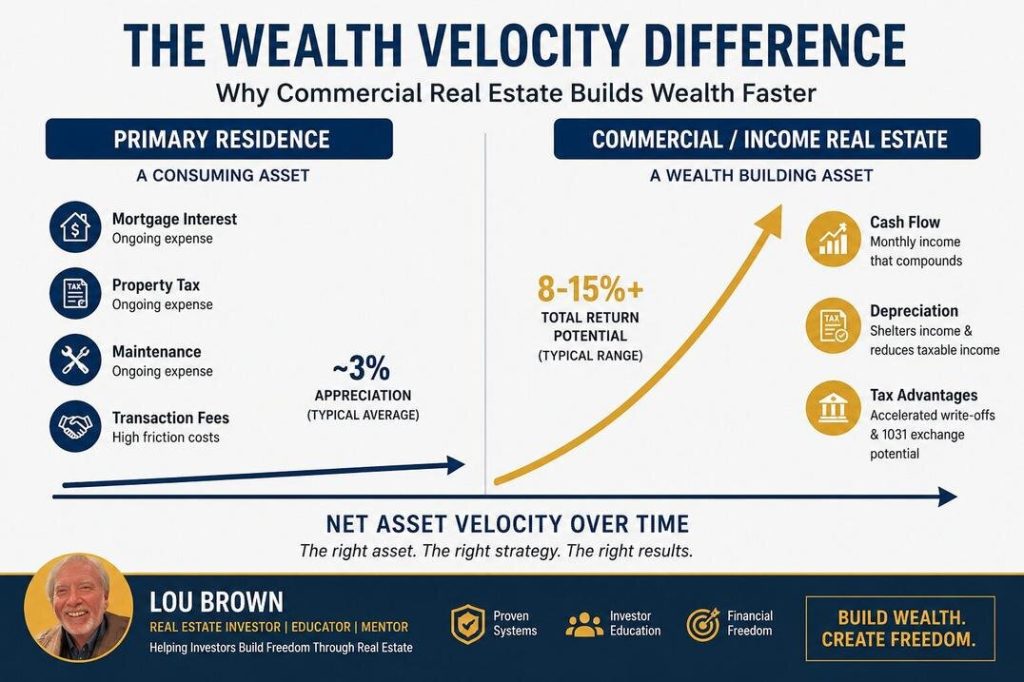

Why Your Primary Residence Is a Wealth Differentiator and Not a Liquid Investment

Our culture treats the family home as the crown jewel of personal finance. Paul and I pushed back on that, hard.

Your house is not an investment. The house that you live in is not an investment. Statistically, homes appreciate about 3% a year, and so that is not an investment. Treat your home as basically an investment so that you have that awareness and that mindset.

Once you factor in mortgage interest, property taxes, maintenance, inflation, and the transaction fees baked into every buy and sell, that modest appreciation rarely beats a dedicated commercial investment or a business.

This lines up with long-run housing data, including the Nobel-winning work behind the Case-Shiller Home Price Index, which shows real residential appreciation hovering near inflation over long periods.

When you reframe your home as a lifestyle expense rather than an active wealth engine, your strategic thinking opens up. You stop over-leveraging on duplicated space, and you route that capital into high-yield, tax-advantaged real estate that actually moves the needle for your family’s legacy. Paul shared a sharp example of this in practice.

Paul digs into mindset shifts like this often in his newsletter, The Entrepreneur’s Family Office, which is worth a look if you want his thinking between episodes.

Avoiding Beginner Real Estate Pitfalls by Prioritizing Cash Flow and Bookkeeping

When I asked Paul what he would tell a brand-new investor, he did not hesitate.

“Two things come to mind when looking back. One is bookkeeping, so having an understanding of your cash flow, your reserves, and all financial things. If you don’t have that, you’re floating on ego, and your ego doesn’t pay the bills. You also can’t invest based on your ego. The other thing is really taking action when you can. Real estate is more of a wealth preservation and wealth differentiator than a cash-flow tool to retire or leave your corporate job. The easiest way to have immediate cash flow is through a business. Real estate is a long game, and I didn’t realize how long a game it was.”

You cannot run a real estate business out of a shoebox or a single checking account. Assuming a property is profitable based on gross numbers leaves you exposed the moment a real cost lands. A failed HVAC system, a roof replacement, or a long vacancy can erase years of unmonitored cash flow if you have no reserves set aside.

Marketing is the engine that makes your phone ring with motivated sellers, and I break down exactly how to do that in my article on why marketing is the key to the success of your real estate business.

This is exactly the gap real estate wealth preservation is meant to close. Real estate forgives plenty of mistakes over a ten to twenty year horizon, but only if you stay disciplined in the short term. Build bulletproof bookkeeping, hold strict cash reserves, and treat every property with the structural rigor of an enterprise business. Paul learned this the expensive way through a cash-out refinance, which he ended up living off of instead of reinvesting, and you can hear more of his perspective on that on his LinkedIn page. For investors who want to pressure-test deals before buying, BiggerPockets offers free rental property calculators that bake in reserves and capital expenditures.

How This Conversation Reshaped My Strategy on Real Estate Capital Allocation

Paul closed with the idea that stuck with me the longest.

“The most incredible, wonderful, and amazing experiences in my life have been unexpected. And so then, who am I to know exactly how it’s supposed to work? The two things you can control are attitude and action. Keeping up with the Joneses is the most expensive thing that you could ever really have. A home is still a home whether you own it or not, and we just don’t need that much space or that much stuff, really.”

Reflecting on our time together, I keep coming back to one question: what are we actually optimizing for? This conversation reinforced my belief that investors have to separate their desire for status from their math.

I focus on capital allocation to maximize impact and use tax law to protect profits. True financial freedom comes from not comparing yourself to others, mastering financial frameworks, and building a real estate machine that supports your goals.

Want to go deeper on active versus passive losses, short-term rental tax strategies, and the mindset shift that changed how I think about capital allocation? My full conversation with Paul Graham covers all of that and more.

Frequently Asked Questions

How do high-income earners use real estate to lower their tax bracket?

High-income earners lean on strategies like short-term rentals with material participation or Real Estate Professional Status. These approaches let investors classify real estate depreciation and losses as active, which can then legally offset corporate W-2 salaries or business revenue rather than being trapped against passive income alone.

What is the difference between active and passive losses according to the IRS?

The IRS sorts income and losses into separate buckets. Passive losses, which come from traditional rentals where you do not materially participate, can only offset passive income. Active losses, which come from businesses you run, oil and gas investments, or short-term rentals you actively manage, can offset active income such as wages and bonuses.

Why is a primary residence traditionally not considered an investment?

A primary residence generates ongoing non-deductible costs like maintenance, insurance, and property taxes without producing monthly income. Because standard homes historically appreciate close to the rate of inflation, the net return after transaction and holding costs rarely qualifies as a true wealth generator compared with commercial or income-producing real estate.

Apply as a Guest Speaker

The real estate landscape is shifting fast, tax codes keep evolving, and real wealth preservation takes more than generic financial advice. If you are actively working in the industry, executing creative tax strategies, or solving real housing problems across brokerage, development, or finance, we want to feature your expertise on the show.

Marigona Gllarevaa – Jan 01, 1970